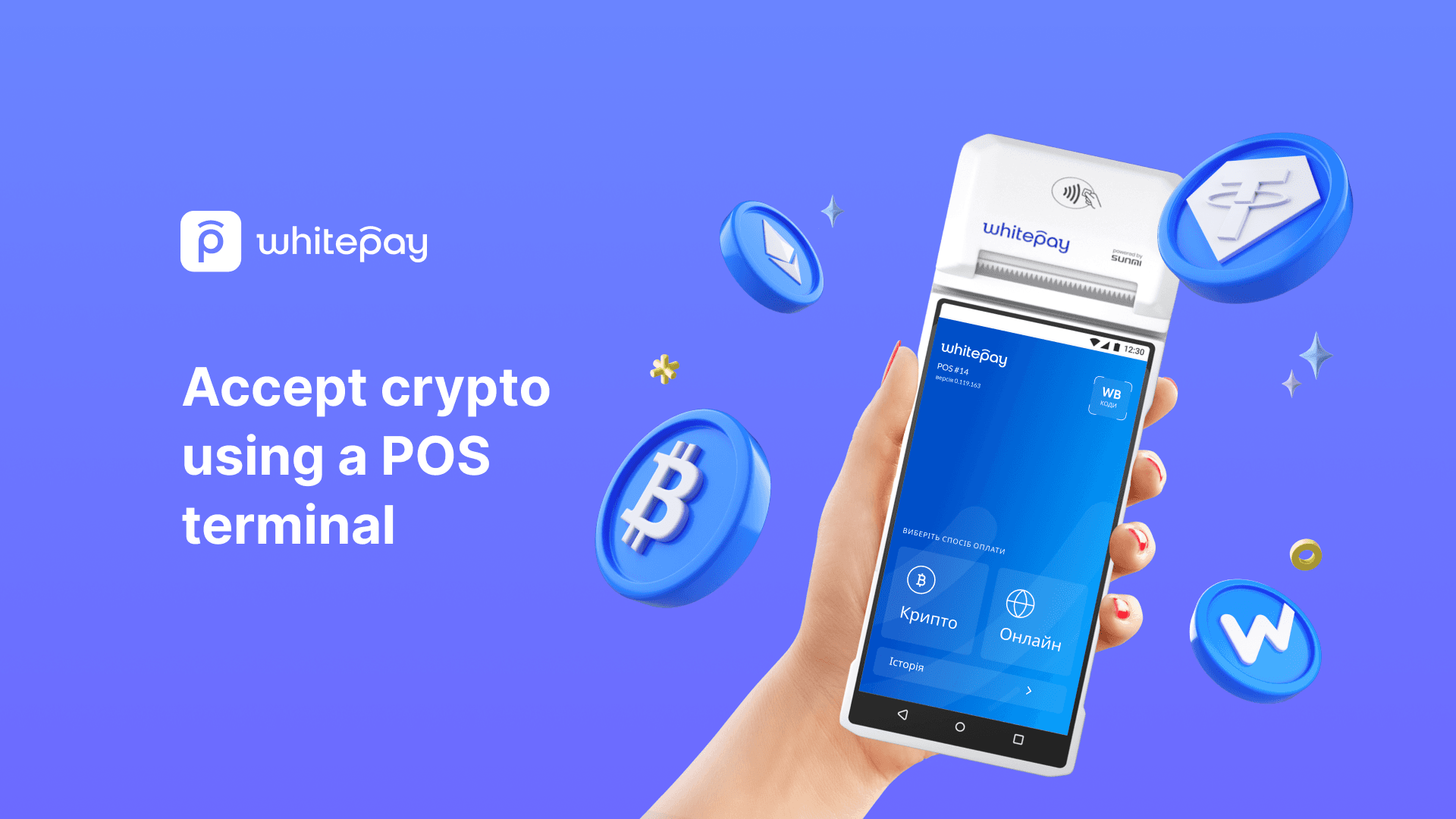

In 2026, private stablecoin cards stand out as the quiet revolution in crypto off-ramps, letting you spend USDT or USDC at any Visa or Mastercard terminal without the usual fiat conversion headaches. These crypto off-ramp cards bridge the blockchain to everyday purchases, keeping your transactions swift and discreet. Imagine loading your stablecoins from Ethereum, Solana, or Tron, then paying for coffee or flights seamlessly; the chain works invisibly behind the scenes. With firms like Rain exploding - their active card base up 30-fold last year and payment volume surging nearly 40 times - adoption is no longer niche. This shift promises faster settlements and lower costs than banks, empowering users who value control over their digital assets.

Industry watchers from Flourish Ventures call it the beginning of the end for traditional ramps. Platforms like Rain, Bridge, and Kulipa now enable direct stablecoin spending, turning what was once a clunky process into something as simple as tapping your phone. For privacy advocates, these private stablecoin debit cards shine by minimizing exposure; many operate with enhanced anonymity features, sidestepping full KYC where possible. No more waiting days for bank wires or fretting over exchange fees - just fluid movement from chain to real-world value.

Unlocking Frictionless Off-Ramps with Stablecoin Power

The genius of stablecoin cards lies in their dual-edge efficiency: they handle the bank side and the chain side effortlessly. Sources like Crypto Adventure highlight the 'Two-Edge Problem, ' where legacy ramps falter on speed or compliance. Private cards solve this by partnering with networks like Visa and Mastercard, converting stablecoins on-the-fly at point-of-sale. CoinGecko's top 10 crypto cards for 2026 emphasize debit modes for EUR, GBP, USD stablecoins, even with daily compound interest perks for holders.

Take Rain: supporting major stablecoins across multiple chains, it has become a fintech powerhouse. PYMNTS notes how stablecoins mimic digital cash, enabling direct transfers and easy cash-to-chain conversions via partners like Coinme. This matters for users dodging volatility; your USDC stays pegged, ready for instant spending. Risks? Minimal if you stick to regulated issuers, but always verify reserves and smart contract audits - a habit from my FRM days.

Privacy Meets Practicality in Non-KYC Spending

For those chasing anonymous crypto fiat conversion and non-KYC stablecoin spending, private stablecoin cards deliver without compromise. Unlike full-service exchanges demanding endless docs, these cards often onboard via wallet connects or minimal verification, preserving your edge. Insights4vc spotlights Coinbase Visa debit, Binance Card, Crypto. com Visa, and Gemini Mastercard as frontrunners, alongside wallet-based options. Bleap's guide on best on/off-ramps in 2026 underscores off-ramps for card spending over bank pulls, cutting intermediaries.

Top Advantages of Stablecoin Cards

- Instant POS Conversions: Spend USDT or USDC directly at terminals with invisible blockchain processing for seamless, real-time payments.

- Multi-Chain Support: Works across ETH, SOL, TRX, and Stellar, as with Rain's platform.

- Enhanced Privacy: Low/no KYC options keep transactions private and user data minimal.

- Global Visa/MC Acceptance: Use anywhere Visa or Mastercard works, via Rain, Crypto.com, or Coinbase cards.

- Earn Yields on Balances: Gain daily compound interest on stablecoin holdings while spending freely.

Zengo's stablecoin wallet insights add fiat on-ramps via cards or transfers, but the real win is 24/7 support baked in. Defiprime's stablecoin issuance map details regulatory frameworks ensuring stability, from technical stacks to providers. In practice, this means loading USDT from your wallet, then off-ramping privately at any merchant - no traces back to your full identity.

Navigating the 2026 Landscape of Top Cards

Shareuhack's 2026 crypto card guide tiers them from S-Tier 'god cards' to curiosities, defining stablecoin crypto cards as Visa/Mastercard tools for USDT-like spending. Polygon Labs praises Coinme for closing the 'last mile' with compliant ramps linking cash, cards, and chains. As a risk specialist, I advise prioritizing cards with proven audit trails and diversified chain support to mitigate single-point failures.

Read more on how stablecoin cards revolutionize off-ramps. These tools aren't just convenient; they redefine financial sovereignty, letting you control risk while unlocking potential in a borderless economy.

Yet sovereignty comes with choices, and selecting the right private stablecoin debit card demands a clear-eyed look at fees, limits, and chain compatibility. Crypto Adventure's breakdown of 2026 debit cards reveals FX spreads as low as 0.5% on premium tiers, with daily limits pushing $10,000 for verified users. This efficiency crushes traditional off-ramps, where wires drag on for days amid 2-5% bites.

Comparison of Top 2026 Stablecoin Cards 🏆

| Provider | Supported Chains (ETH/SOL/TRX) | FX Fee | Daily Limit | Privacy Level (Low/Med/High KYC) |

|---|---|---|---|---|

| Rain 🌧️ | ETH✅ SOL✅ TRX✅ | 0.5% 💰 | $100,000+ | High (Low KYC) 🔒 |

| Coinbase Visa 💳 | ETH✅ SOL❌ TRX❌ | 1.5% | $10,000 | High KYC 📋 |

| Crypto.com Visa 🅿️ | ETH✅ SOL✅ TRX✅ | 1% | $50,000 | Med KYC ⚖️ |

| Binance Card 🐾 | ETH✅ SOL✅ TRX✅ | 0.9% | $25,000 | High KYC 📋 |

| Gemini Mastercard ⭐ | ETH✅ SOL✅ TRX❌ | 1.2% | $20,000 | High KYC 📋 |

From my vantage as a risk manager, Rain edges out as a standout for its multi-chain prowess and explosive scaling, but diversify: pair it with a wallet like Zengo for backup on-ramps. Shareuhack's tier list dubs these S-Tier when they blend yields - think 4-6% APY on idle USDC - with global reach. Defiprime's issuance map reassures with frameworks like EU MiCA compliance, fortifying peg stability amid market whims.

Risk Management Essentials for Everyday Users

Don't let the seamlessness lull you; smart protocols keep your edge sharp. Prioritize cards audited by firms like PeckShield or Certik, ensuring reserves match 1: 1. I've seen depegs wipe gains overnight, but battle-tested stablecoins like USDC hold firm under scrutiny. For anonymous crypto fiat conversion, opt for non-custodial loads from your wallet, minimizing counterparty risk. Coinme's 'last mile' model via Polygon bridges cash to chain compliantly, ideal for hybrid users blending physical and digital flows.

Regulations evolve fast - 2026 brings clearer U. S. stablecoin bills - so geo-check availability. In Europe, Kulipa and Bridge thrive under PSD3, slashing cross-border frictions. My advice: start small, monitor via apps with real-time proofs, and rotate issuers quarterly. This layered approach mirrors FRM principles: identify threats early, hedge exposures, thrive long-term.

Real-World Wins and Getting Started

Users report ditching bank cards entirely; one Rain holder swiped $5,000 monthly across continents with zero declines. PYMNTS captures this as digital cash reborn, fueling peer-to-peer speed without ledgers exposed. For businesses, Zengo's wallets scale to treasury ops, onboarding via bank transfers while cards handle outflows.

Explore deeper in how stablecoin cards enable instant off-ramping without KYC. Platforms like anonofframp. com streamline this further, pairing cards with private on/off services for the full loop.

These cards aren't a fad; they're the infrastructure for tomorrow's finance, where privacy and speed coexist. Load up, spend freely, and watch traditional barriers crumble - you've got the tools to navigate with confidence.

No comments yet. Be the first to share your thoughts!