Stablecoin cards have rapidly shifted from a niche innovation to a mainstream financial tool, fundamentally altering how users bridge the gap between crypto and fiat in 2024. As real-world use cases for digital assets expand, these cards are setting a new standard for on/off-ramp efficiency, privacy, and global reach.

Why Stablecoin Cards Are Disrupting On/Off-Ramp Payments

Historically, moving funds between crypto and traditional finance was slow, expensive, and often required intrusive KYC checks. Stablecoin payment cards are changing that equation. By letting users spend stablecoins like cash anywhere Visa or Mastercard is accepted, these cards bypass legacy bottlenecks while preserving the speed and transparency of blockchain rails.

The market has seen explosive growth in 2024, with major launches like the KAST Card (supporting USDC, USDT, and USDe across multiple blockchains) and Visa’s partnership with Bridge targeting Latin America. These solutions allow users to top up with stablecoins and spend globally at over 100 million merchants, no conversion headaches or hidden fees.

This isn’t just about convenience. For privacy advocates and crypto natives alike, platforms such as anonofframp. com offer private crypto cards that minimize personal data exposure while maximizing transaction speed.

The Key Players: Market Leaders Defining the Space

The competitive landscape is heating up. According to Mural Pay’s latest rankings for 2025, providers like Mural Pay itself, Circle, Bitso, Ripple (especially after acquiring Rail), Mercado Pago, and Banxa are setting the pace for fast crypto-to-fiat conversion. Meanwhile, Offramp. xyz is attracting attention by offering instant virtual cards with zero setup or maintenance fees, a major draw for both new adopters and high-frequency users.

The most widely-used stablecoins remain USDT, USDC, and DAI, but emerging options like USDe and PYUSD are gaining traction as payment networks expand their integrations. Visa’s own research calls stablecoins "fast, borderless and accessible, " underscoring their potential to disrupt incumbent payment systems at scale.

How Stablecoin Cards Work: Under the Hood of Instant Crypto-to-Fiat Conversion

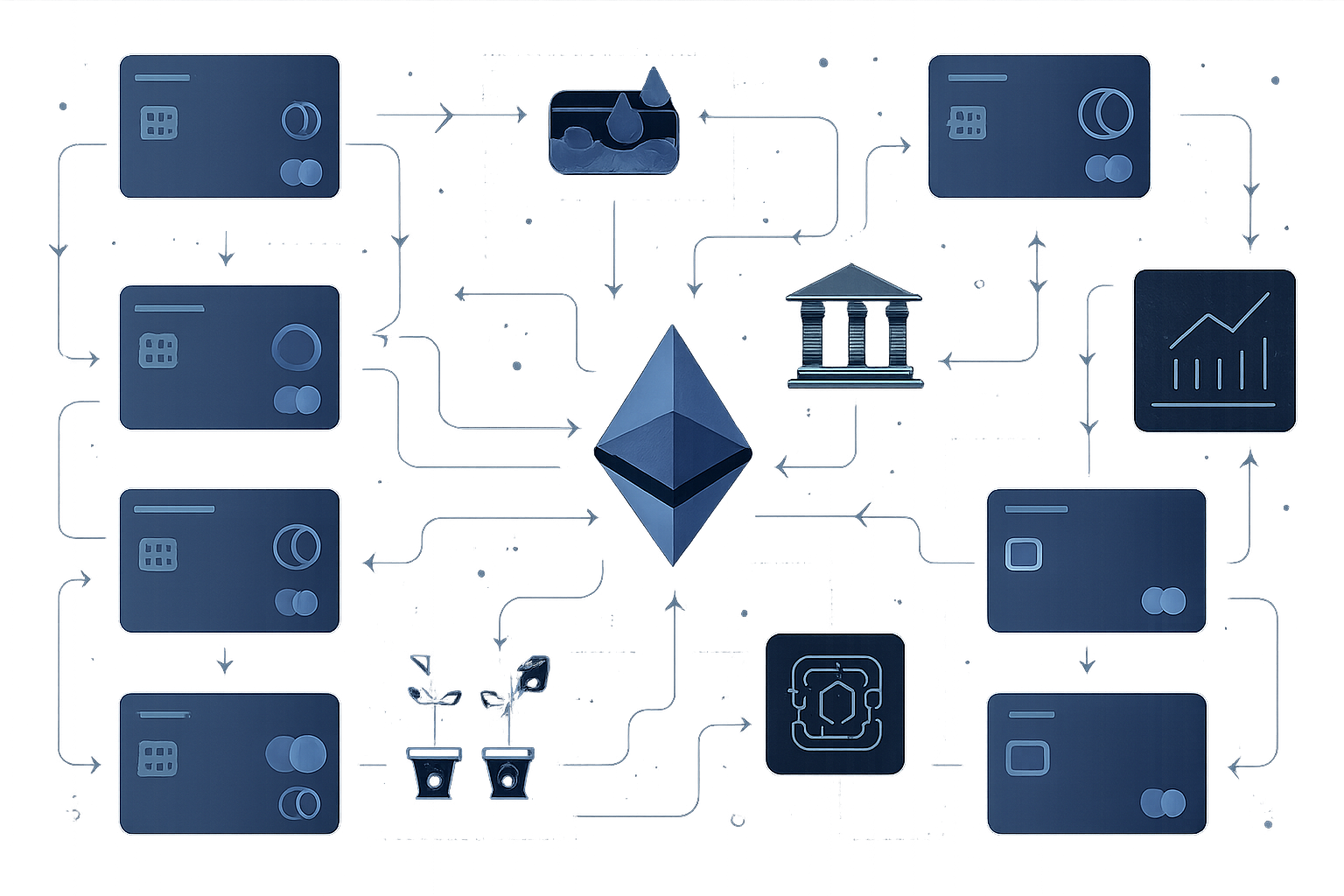

A typical stablecoin debit card works by linking your crypto wallet to a card account. When you make a purchase at any supported merchant, whether online or in-store, the backend converts your chosen stablecoin (like USDC or USDT) into local currency in real time. This process leverages robust APIs from partners such as Bridge (for Visa) or Onramper (for Helio), ensuring transactions clear instantly without manual swaps or delays.

This architecture brings several advantages:

- No need for centralized exchanges: Users avoid lengthy withdrawal processes or off-ramp bottlenecks.

- Tighter privacy controls: Many providers offer minimal KYC onboarding or even anonymous usage tiers.

- Lower fees: By cutting out banking intermediaries, transaction costs drop significantly compared to legacy methods.

- Bigger reach: Spend your digital assets at millions of merchants worldwide, no more limits on where your crypto can go.

This seamless experience is why more merchants are embracing stablecoin payments as part of their checkout options, a trend expected to accelerate into 2025 as regulatory clarity improves globally. For an in-depth look at technical mechanics behind these cards, see our feature on how stablecoin cards work worldwide.

Security and user control are front-and-center as stablecoin card adoption grows. Most leading cards now offer advanced fraud protection, instant transaction alerts, and the ability to freeze or unfreeze cards directly from a mobile app. This is a major upgrade from legacy debit cards, where users often wait days for issue resolution. With stablecoin payment cards, you’re in the driver’s seat, manage your funds 24/7, monitor spending in real time, and keep your crypto assets safe from unauthorized access.

For privacy-focused users, platforms like anonofframp. com are leading the charge by offering stablecoin debit cards with minimal data requirements. These solutions attract users who want to avoid traditional KYC friction while still enjoying global payment capabilities. The result: a powerful blend of privacy and compliance that’s redefining what “bankless” finance means in 2024.

What Sets 2024’s Stablecoin Cards Apart?

The latest generation of stablecoin cards goes beyond simple spending. Many now support multi-chain top-ups (including Ethereum, Solana, Tron), dynamic rewards (like KAST’s SOL staking bonuses), and even DeFi yield integration. Imagine topping up your card with USDC on Polygon, earning cashback in crypto, and instantly spending at any point-of-sale terminal worldwide, all without touching a centralized exchange or banking app.

This convergence of DeFi and payments is accelerating thanks to strategic partnerships, Ripple’s acquisition of Rail turbocharged its cross-border payout engine, while Helio x Onramper is making fiat-to-stablecoin onboarding frictionless for merchants across continents.

The Road Ahead: Stablecoin Cards as a New Financial Primitive

Looking forward into 2025 and beyond, expect stablecoin payment cards to become a default on/off-ramp for both individuals and businesses. Payroll disbursement in USDC or USDT is already gaining traction among remote teams; cross-border freelancers can now receive payments instantly without waiting for slow wire transfers or losing value to FX fees. Even B2B settlements are moving onto blockchain rails as corporate treasuries look for faster cash flow cycles.

Regulatory clarity remains an evolving challenge, particularly around privacy tiers, but the momentum is clear: Stablecoin debit cards are here to stay, pushing crypto adoption from speculative trading into everyday finance at scale.

If you want more details on how these innovations work under the hood or wish to compare top providers side by side, check out our practical guide on how stablecoin cards are changing crypto payments.

No comments yet. Be the first to share your thoughts!