Choose your off-ramp route

Selecting the right method to convert cryptocurrency to fiat depends on your priority: speed, cost, or privacy. There is no single best option; each route involves a trade-off between convenience and expense. You must weigh how quickly you need the funds against the fees you are willing to pay.

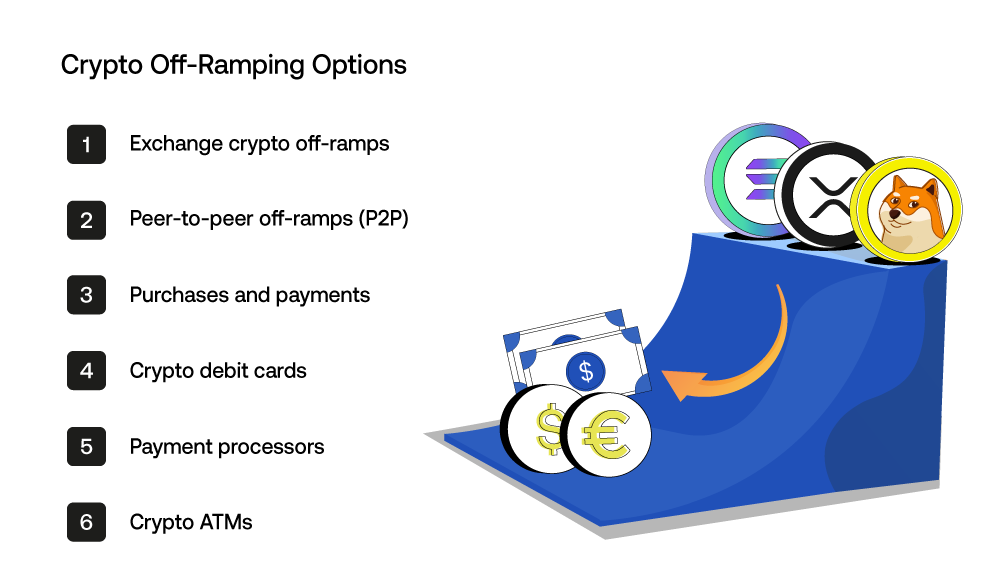

The four main off-ramp routes in 2026 are centralized exchanges, dedicated fintech apps, peer-to-peer (P2P) networks, and crypto debit cards. Centralized exchanges (CEXs) like Coinbase or Binance offer the lowest fees but require full KYC verification and take 1–3 days for bank transfers. Fintech apps like MoonPay or Transak provide instant settlement to debit cards but charge premiums of 1–4% for the convenience. P2P platforms allow direct transfers between users, offering more privacy but carrying higher counterparty risk. Crypto cards let you spend directly, effectively off-ramping at the point of sale, though they often include foreign transaction fees.

| Route | Typical Fee | Settlement Time | KYC Required | Privacy Level |

|---|---|---|---|---|

| Centralized Exchange (CEX) | 0.1% – 0.5% | 1–3 business days | Yes | Low |

| Fintech App (Debit Card) | 1% – 4% | Instant to 24h | Yes | Low |

| Peer-to-Peer (P2P) | 0% – 2% | 15 mins – 24h | Varies | Medium |

| Crypto Debit Card | 1% – 3% | Instant (at POS) | Yes | Low |

Centralized Exchanges (CEXs)

CEXs are the most established off-ramp method. You sell crypto for fiat on the platform, then withdraw to your linked bank account via ACH or wire transfer. This route is best for large sums where minimizing fees is critical. However, you must complete identity verification, and bank transfers are not instant. Use this if you prioritize low costs over speed.

Fintech Apps and Debit Cards

Fintech platforms integrate directly with card networks. You convert crypto to fiat instantly, which is then loaded onto a prepaid or linked debit card. This is ideal for immediate spending needs. The trade-off is higher fees, often including a spread on the exchange rate. Use this if you need funds available within minutes.

Peer-to-Peer (P2P) Networks

P2P platforms connect buyers and sellers directly. You can receive bank transfers, cash deposits, or other payment methods. This route offers more flexibility and potentially lower fees than fintech apps, but it requires manual verification of the counterparty. Use this if you want to avoid platform holds or need specific payment methods.

Pre-Off-Ramp Checklist

Before initiating any conversion, ensure your account is fully verified and your bank details are correct. Check the daily withdrawal limits of your chosen platform. Confirm that your bank supports incoming transfers from crypto-related entities, as some institutions block these transactions.

-

Verify identity documents are up to date on the platform

-

Confirm bank account details match the registered name

-

Check daily withdrawal limits and fees

-

Ensure your bank accepts crypto-related transfers

-

Review tax reporting requirements for the transaction

Execute the conversion via exchange

Selling your crypto on a regulated exchange is the most reliable way to off-ramp digital assets into your bank account. This method offers institutional-grade security and clear audit trails, which are essential for tax compliance. Unlike peer-to-peer deals, centralized exchanges handle the fiat settlement through established banking rails, reducing the risk of frozen accounts or chargebacks.

The process follows a straightforward sequence: verify your identity, sell the asset, and withdraw the fiat proceeds. While the steps are simple, each stage requires attention to detail to ensure funds arrive correctly and legally.

Before you can move money, you must prove who you are. Regulated exchanges require Know Your Customer (KYC) verification to comply with anti-money laundering laws. This involves submitting government-issued identification and sometimes proof of address. Without a verified account, you cannot link a bank account or withdraw fiat. This step is non-negotiable for legal off-ramping.

Connect your bank account using the exchange’s secure portal. Most platforms use ACH (in the US) or SEPA (in Europe) for low-cost transfers. You may need to verify small test deposits to confirm ownership. Ensure the name on the bank account matches the name on your exchange account exactly. Mismatches often trigger security holds that delay withdrawals by days.

Navigate to the trading interface and sell your cryptocurrency for your local currency (e.g., USD, EUR). You can use a market order for immediate execution at the current price or a limit order to set a specific price. Be aware of trading fees, which vary by platform and asset. Once the trade settles, your account balance will reflect fiat currency rather than digital tokens.

Initiate a withdrawal from your exchange balance to your linked bank account. Choose ACH for lower fees (typically 1-3 business days) or wire transfer for larger sums (often same-day but with higher fees). Double-check the withdrawal amount and destination account. The funds will appear in your bank statement as a deposit from the exchange, not a direct crypto transfer.

Timing your withdrawal can impact your net proceeds. Market volatility affects the value of your crypto before the sale, while banking delays can affect when you actually access the funds. For large amounts, consider splitting the withdrawal into smaller chunks to stay within daily banking limits and reduce exposure to price swings.

Always keep records of your transaction IDs and trade confirmations. These documents serve as proof of sale for tax reporting purposes. Exchanges provide annual tax forms, but maintaining your own records ensures accuracy if you need to reconcile discrepancies later.

Handle tax reporting and compliance

Off-ramping cryptocurrency is not just a financial transaction; it is a taxable event. The IRS treats crypto as property, meaning every time you sell, trade, or spend it, you trigger a capital gains tax liability. Failing to report these transactions can lead to audits, penalties, and interest charges that far exceed the tax owed.

Track your cost basis

To calculate your tax liability, you must determine your cost basis—the original value of your crypto when you acquired it. If you bought Bitcoin for $20,000 and sold it for $50,000, your capital gain is $30,000. The IRS uses specific rules to determine which coins are being sold if you hold multiple batches (e.g., FIFO, LIFO, or Specific Identification). Keeping detailed records of every purchase date, price, and transaction fee is essential for accurate reporting.

Report on Form 8949

All crypto sales and exchanges must be reported on IRS Form 8949, "Sales and Other Dispositions of Capital Assets." This form requires you to list each transaction individually, including the date acquired, date sold, proceeds, and cost basis. The totals from Form 8949 then flow to Schedule D of your tax return. Many tax software programs now automate this process by importing data from exchanges and trading platforms, but you are responsible for verifying the accuracy of that data.

Stay compliant with state rules

In addition to federal taxes, some states have their own crypto tax regulations. While most follow federal guidelines, a few states may have different rules regarding reporting thresholds or specific types of transactions. Ensure you are aware of your state’s requirements to avoid unexpected liabilities. Ignorance of the law is not a defense, so proactive compliance is your best protection against legal trouble.

Avoid common off-ramp mistakes

Converting crypto to fiat sounds simple, but a single misstep can freeze your funds or trigger tax audits. Most errors happen during the handoff between the exchange and your bank. Follow these three checks to keep your off-ramp route clean and compliant.

Match bank names exactly

Off-ramp platforms often reject transfers if the recipient name on the exchange doesn’t match the bank account holder. Even a minor typo in the legal name or using a business name for a personal account can cause the bank to return the funds. Always verify the exact legal name registered with your financial institution before initiating the withdrawal.

Watch for hidden fees

Exchange fees are only part of the cost. Many off-ramp routes charge network gas fees for the crypto withdrawal and additional processing fees for the fiat deposit. Some platforms also apply unfavorable exchange rates. Compare the total cost across CEXs, fintech apps, and P2P markets. A slightly higher trading fee might be worth it if the off-ramp path has lower hidden costs.

Verify KYC status early

Regulatory compliance is strict in 2026. If your identity verification is expired or incomplete, your bank account may be flagged or frozen during the transfer. Ensure your KYC documents are up to date on every platform you use. This prevents delays that could leave your funds stuck in limbo while you scramble to update your profile.

No comments yet. Be the first to share your thoughts!